Against this backdrop, in November and December 2022 we fielded responses to inform Lazard’s Healthcare Services Leaders Study 2023. We received input from 150 leaders across many of the largest healthcare services companies, as well as smaller public and private companies and prominent investment firms.

Our Central Findings:

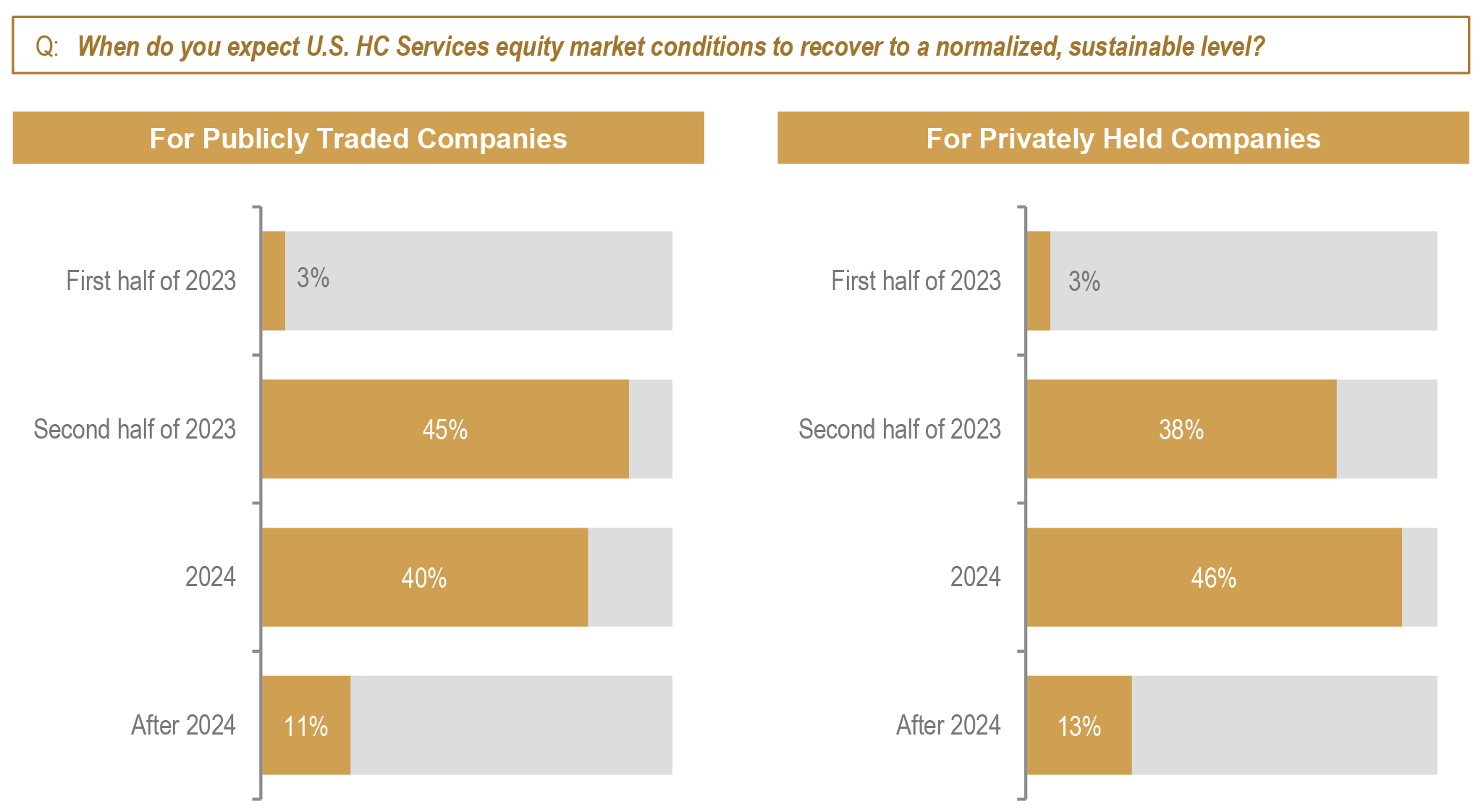

1. Healthcare services equity market conditions are unlikely to recover to normalized, sustainable levels before the second half of 2023. A market recovery will be catalyzed by an improved macroeconomic outlook, greater access to capital, and improved investor sentiment toward sector profitability.

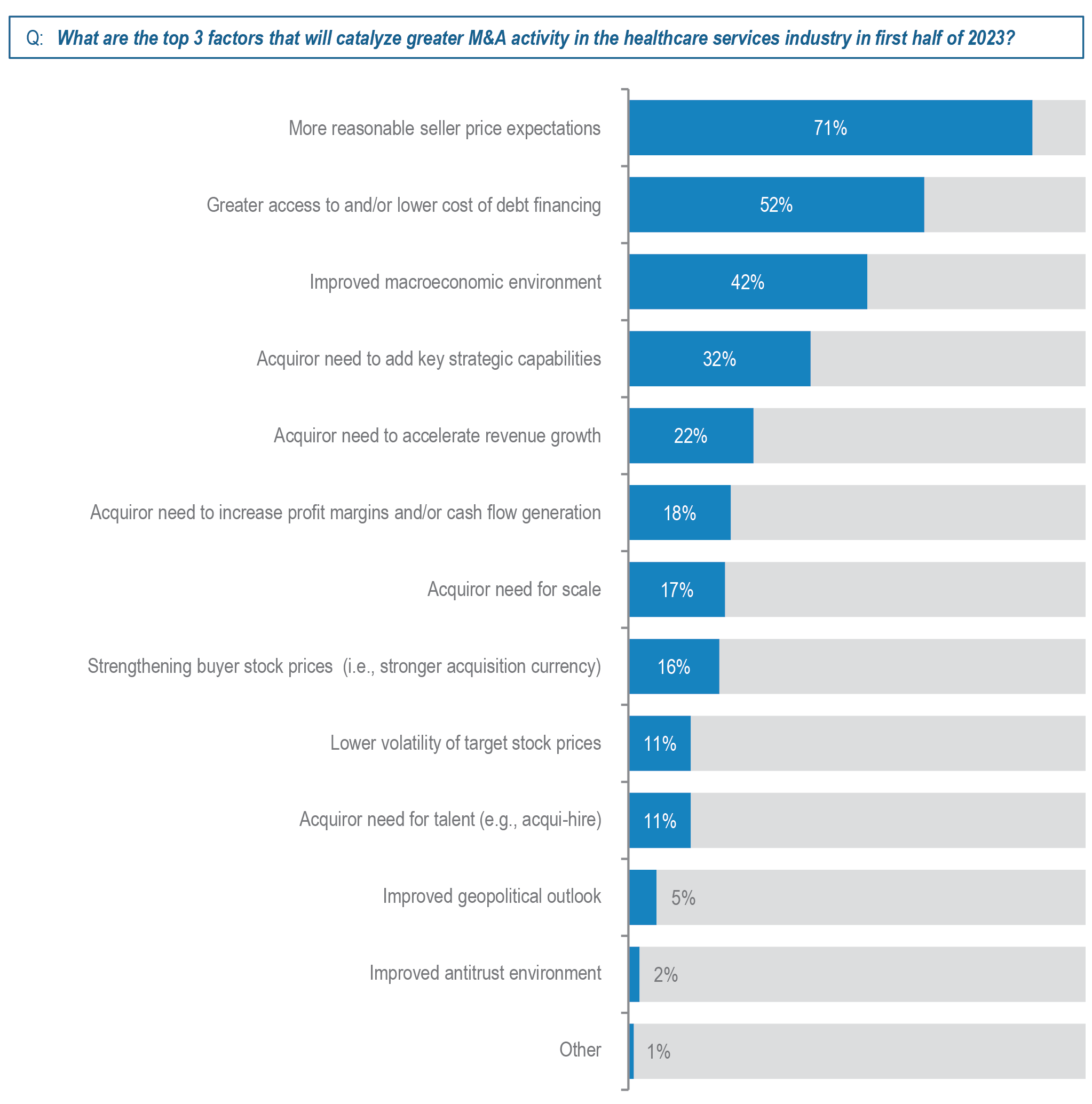

2. While large-cap consolidation is expected to remain at the same relatively low level, bolt-on acquisitions, together with partnerships/collaborations and corporate carve-outs, are expected to increase. Improvements in seller price expectations, the availability of capital, and buyer perceptions of lower risk in achieving forecasts will be important catalysts of rising strategic activity.

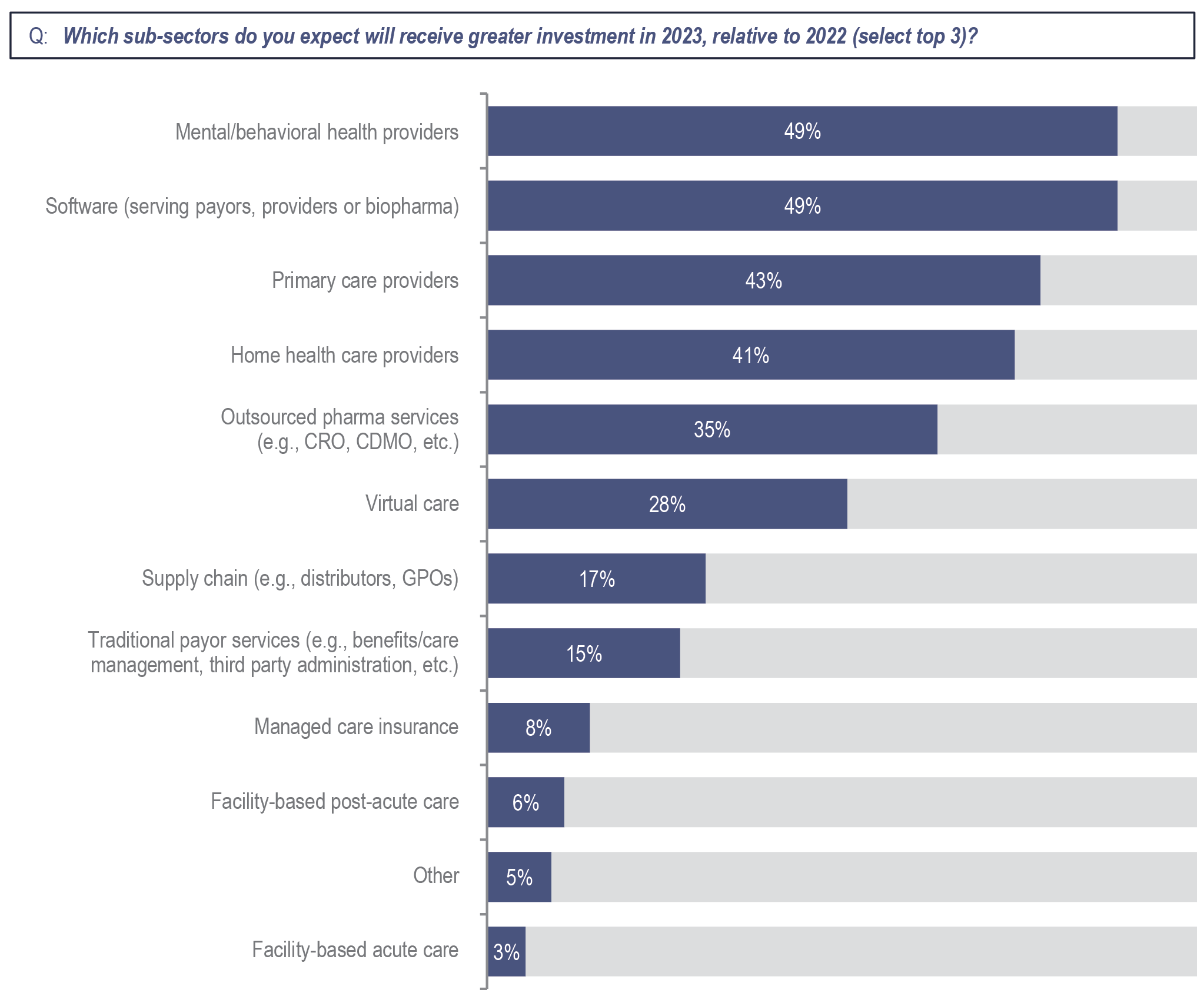

3. Mental/behavioral health, software, and primary care are expected to receive greater investment in 2023 than in 2022, followed by home health and outsourced pharma services. Least likely to receive greater investment in 2023 are facility-based acute and post-acute care and managed care insurance.

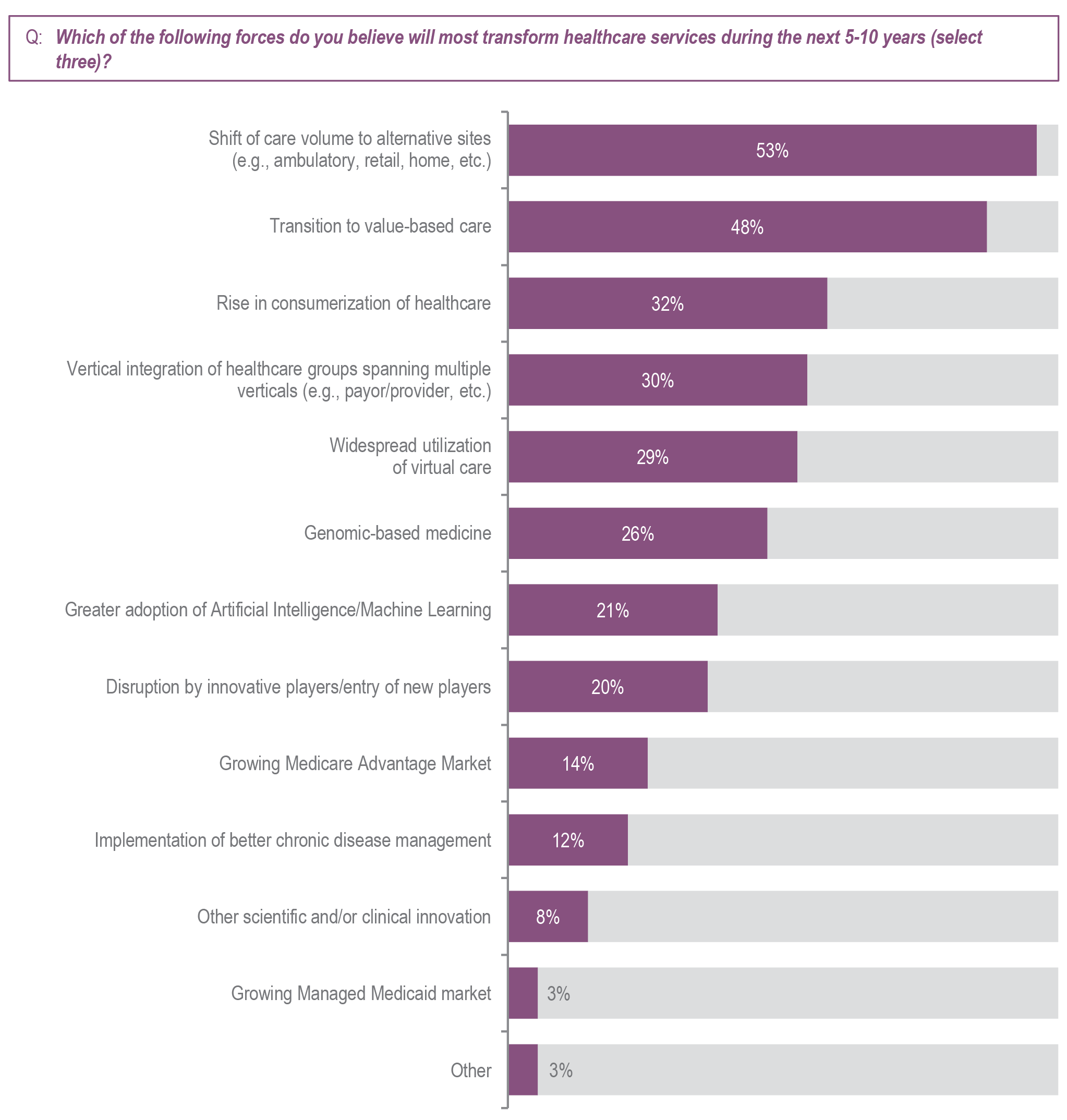

4. The ongoing shift of care volume to alternative sites and the transition to value-based care are the forces expected to most transform healthcare services over the coming decade, followed by a rise in consumerization of healthcare, vertical integration of healthcare groups, and widespread utilization of virtual healthcare.

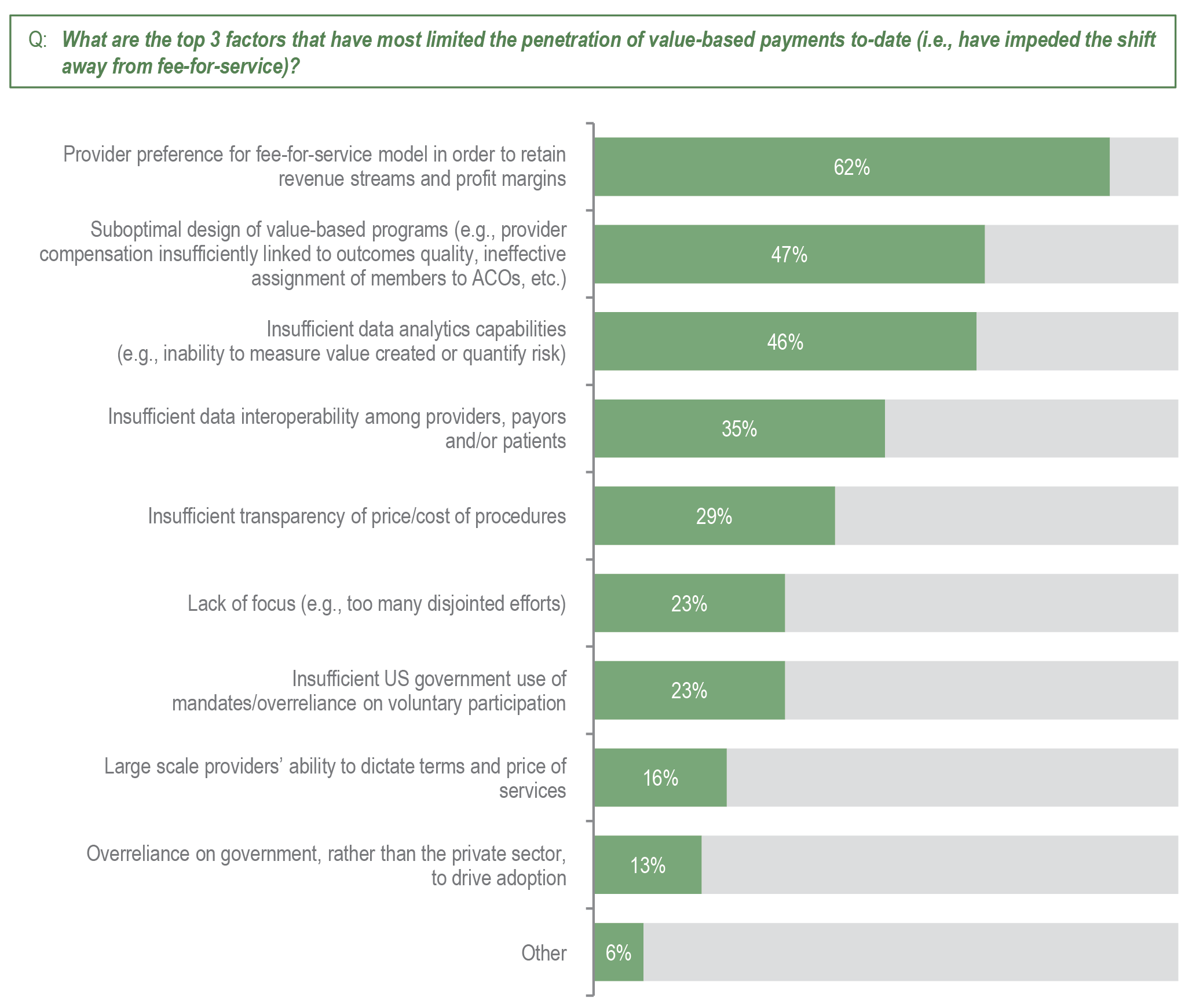

5. Most healthcare services leaders believe that a majority of healthcare payments will be governed by alternative payment models (i.e., value-based care) within the next five years. The transition to value-based care has been most limited by provider preference for fee-for-service reimbursement, suboptimal design of value-based programs, and insufficient data analytics capabilities.